How do you actually collect money online? It sounds like a small question, but it’s the one that slows down more Nigerian sellers than anything else. The wrong setup leads to delayed payments, manual midnight verification, and customers dropping off because checkout is too stressful.

This guide breaks down five proven ways to receive online payments in Nigeria, what each is best for, and the honest trade-offs that most reviews skip.

How to Receive Online Payment in Nigeria in 5 Tested Ways

Not every method works the same way for every seller. Some require a website, some work straight from your phone, and some are better suited to high-volume businesses than to someone just getting started. The five methods below are tested, practical, and clear about what each one costs you in time, fees, or setup effort.

1. Integrate a Payment Gateway

A payment gateway is the most reliable way to receive online payments if you already have a website or plan to build one. It sits between your product page and the customer’s bank, processes the transaction securely, and automatically confirms payment without requiring manual checking.

In Nigeria, Paystack and Flutterwave are the two dominant options. Both support debit cards, bank transfers, USSD, and bank verification number (BVN)-linked payments. Paystack tends to be easier to integrate for beginners, while Flutterwave offers broader support for cross-border transactions if you’re selling to customers outside Nigeria.

What you need to get started:

- A registered business (or at least a BVN and bank account)

- A website with a checkout or product page

- A developer to integrate the gateway, or a platform that does it for you

The main advantage is automation. Once your gateway is live, customers pay, and the money moves without you lifting a finger. The tradeoff is that setup requires some technical work, and transaction fees (typically 1.5% per transaction, capped at ₦2,000 for Paystack) apply to every sale.

If you’re just starting out and don’t have a website yet, skip ahead to Way 2 or Way 5.

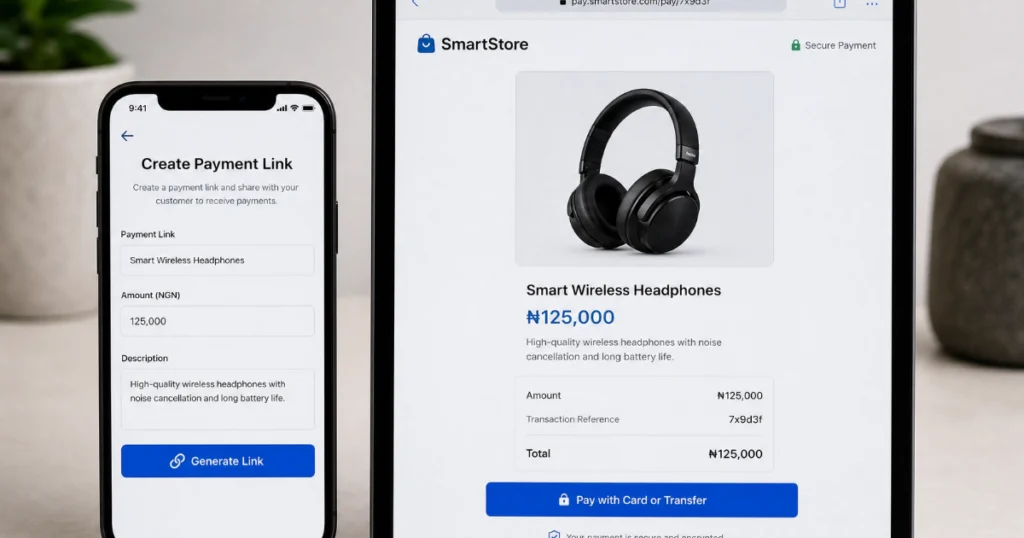

2. Create a Payment Link or Payment Page

You don’t need a full website to receive online payment. A payment page, sometimes called a payment link, is a standalone URL your customers can click to pay you directly.

Both Paystack and Flutterwave let you create a payment page in minutes from your merchant dashboard. You set the amount (or leave it open), add your product name or description, and share the link via WhatsApp, Instagram DM, or email. The customer clicks, pays with their card or via bank transfer, and you get notified instantly.

This is one of the most practical ways for Nigerian Instagram and WhatsApp vendors to move from “send me your account number” to a more professional payment experience without having to build anything technical.

Where it falls short: You still have one product or price per page. If you sell multiple items, you’ll need multiple payment links or a proper storefront. Managing that at scale quickly becomes messy.

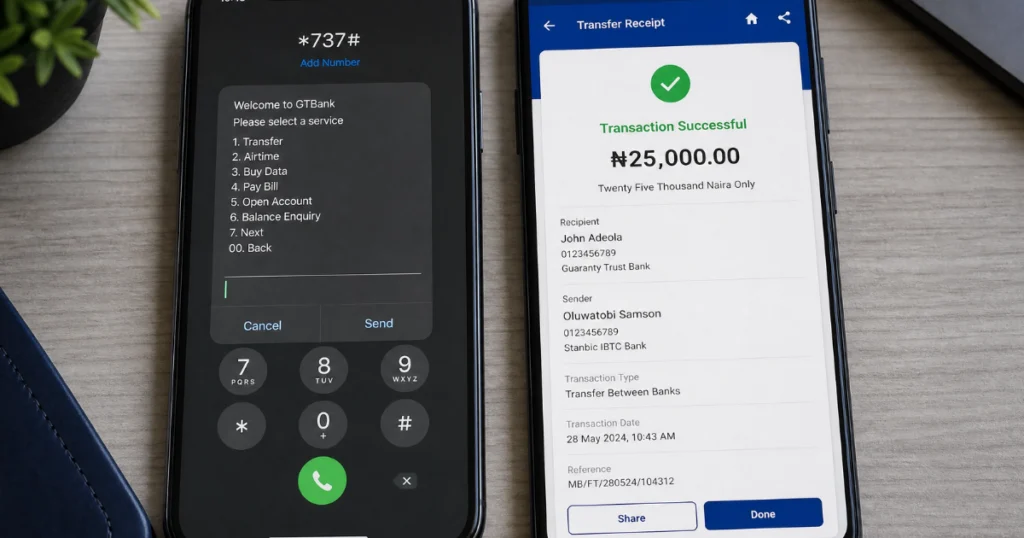

3. Bank Transfer and USSD

This is how most Nigerian sellers started, and honestly, a lot still use it. You share your account number with the customer, they transfer the funds, and you confirm before releasing the product.

It works because nearly every Nigerian with a smartphone can do a bank transfer today via their banking app, USSD code, or at an ATM. There’s no signup, no integration needed, and no transaction fees on your end.

The real downside is that manual payment confirmation means you have to be available and alert. Every order is a DM, a screenshot, a check. At five orders a week, it’s manageable, and anything larger than that gets messy.

There’s also the issue of fraud. Fake credit alerts are a real threat in Nigeria. Sellers have been defrauded by customers who send edited screenshots or USSD “confirmation” texts. Before relying on bank transfer as your primary method, make sure you verify it directly in your banking app, never from a screenshot.

Bank transfer works best as a backup option alongside another payment method, especially for customers without a card.

4. Digital Wallets and Mobile Money

Nigeria has a growing number of wallet platforms, such as OPay, Kuda, and PalmPay, that allow customers to send money directly from one app to another. Some sellers, especially those selling in high-traffic WhatsApp groups or social communities, use their wallet tag or username as a payment option.

The advantage here is speed. OPay-to-OPay transfers, for example, are almost instant and free within the platform. For sellers who have a loyal customer base already on one of these apps, it significantly reduces the friction of bank transfers.

The only downside is thatnot all your customers will be on the same wallet. And like bank transfers, you’re still confirming payments manually. Wallets also don’t integrate cleanly into a checkout flow the way payment gateways do.

Think of wallets as a supplement, not a system. They work when your customer base is already concentrated on a specific platform, but they won’t scale with your business on their own.

5. Receive Payments Through a Marketplace or Storefront Platform

A marketplace or storefront platform handles payment collection on your behalf. Your products are listed, your customers check out, and payment flows to you automatically. No gateway integration, no manual confirmation, no risk of fake alerts. The infrastructure is already built.

Platforms like Jumia exist in Nigeria, but they come with trade-offs such as steep seller fees, limited product control, and a brand experience that belongs to the platform, not to you. Your customer shops on Jumia, not from your store. That makes it harder to build repeat buyers or grow a brand in the long term.

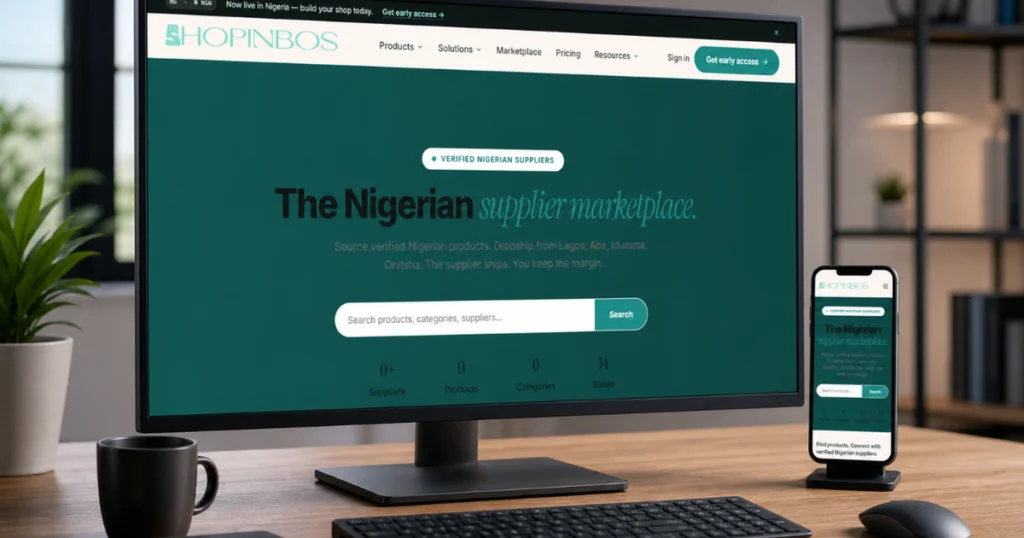

This is where Shopinbos does something different.

The Shopinbos marketplace is a commerce platform built specifically for Nigerian sellers and it combines the parts of the process that usually require multiple tools: an online storefront, access to a verified supplier marketplace, integrated payments via Paystack, bank transfer, cash on delivery, and wallet, and a logistics network covering 14 cities.

What that means in essence is you can build your online store, list products sourced from verified Nigerian suppliers, and start receiving payments all from one dashboard, without hiring a developer or figuring out which payment gateway to integrate.

Other platforms let you choose between a storefront and a marketplace. Shopinbos connects both, so when a customer buys from your store, the order goes to the supplier, the supplier ships, and payment settles to you without the back-and-forth of manual coordination.

Shopinbos simply combines all five ways you can accept payments online into one.

Which Online Payment Method Is Right for You?

Before you choose, ask yourself three questions: Do you have a website already? How many orders do you expect per week? How much time are you willing to spend confirming payments manually?

If you’re building a proper website with a developer, integrate a payment gateway from the start, selling via WhatsApp or Instagram and want something quick, a payment link gets you live in under 10 minutes. If you’re looking for a full setup that includes store, products, payment, and delivery, a platform like Shopinbos is built for exactly that.

Bank transfer and wallets still have a place, but they work best as secondary options, not your primary payment method.

Conclusion

Knowing how to receive online payments in Nigeria is no longer optional; it’s what separates a seller who converts from one who’s still asking customers to “send me your bank details.” The right setup depends on where you are in your business journey, but the important thing is to move from manual to automatic as early as possible.

If you’re just starting out and want the full setup without the stress, explore the Shopinbos storefront builder, where you get products, payments, and logistics in one place.

And while you’re setting up your business, you can also use the free invoice generator to send professional payment requests to customers while your checkout is getting ready.

FAQs on How to Receive Online Payment

The five main ways are: integrating a payment gateway, using a payment link or payment page, collecting via bank transfer or USSD, using a mobile wallet, and selling through a marketplace or storefront platform that handles payment for you. Which one works best depends on your business stage, your tech comfort level, and how much manual work you’re willing to handle per order.

For small businesses just starting out, a payment link is the fastest option, no website required. For sellers who want a complete setup with a storefront, products, and automatic payment processing, a platform like Shopinbos is better suited. It removes the need to manage a gateway, a website, and supplier coordination separately.

Yes. You can share a payment link via WhatsApp, Instagram, or email, and customers can pay without visiting a website. Bank transfers also require no website. If you eventually want to scale, building a proper storefront gives you more control and a better customer experience.

The safest way is to confirm payment directly in your banking app or internet banking dashboard, never via a screenshot or a forwarded text message. Using a payment gateway or a platform with automatic settlement eliminates this risk entirely, since the system confirms before you fulfill the order.

Ready to grow your own shop?

Shopinbos is free to start. Rex builds your storefront in 90 seconds, Peggy handles the rest.

Get early access